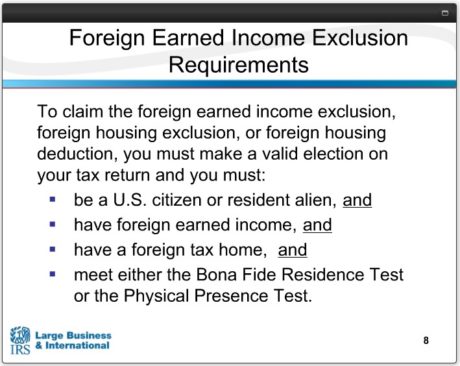

To claim the foreign earned income exclusion, the foreign housing exclusion, or the foreign housing deduction, you must have foreign earned income, your tax sum must be in a foreign country and you must be one of the following: A U.S. resident alien who is a citizen or national — who is a bone fide resident:

⇒ A U.S. citizen who is a bone fide resident of a foreign country or countries for uninterrupted period that includes an entire tax year, a U.S. resident alien who is a citizen or national with country with which the U.S. has an income tax treaty in effect and who is also a bone fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year, or a U.S. citizen or U.S. resident alien who is physically present in a foreign country or countries for at least 330 full days during any period of 12 consecutive months.

The foreign earned income exclusion is voluntary. You can choose the foreign earned income exclusion, the foreign housing exclusion, or both, by completing the appropriate part of Form 2555. Your initial part of the exclusions on Form 2555 or Form 2555-EZ generally must be made with a timely filed return, including any extensions for the due day, a return amending a timely filed return, or a late filed return filed within one year from the original due date of the return determined without regard to any extension.

You can choose the exclusion on a return filed after the periods we just discussed provided you owe no federal income tax after taking the exclusion into account. However, if you owe federal income tax after taking the exclusion into account, you can still choose the exclusion on a return filed after the periods we discussed before, provided you file before the IRS and you failed to choose the exclusion. You must type or legibly print at the top of the first page of your Form 1040 that is filed for pursuant to Section 1.911-7(ea)(2)(i)(d), and the information about this is also in the instructions of the Form 2555.

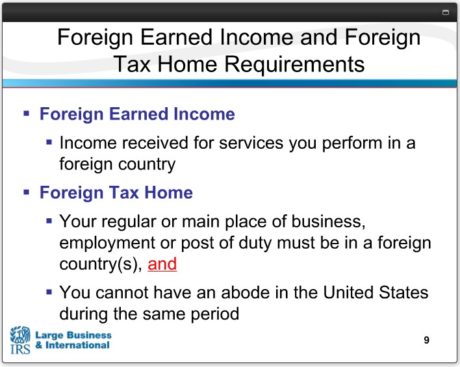

To claim the foreign earned income exclusion, the housing exclusion, or the housing deduction, you must have foreign earned income. Foreign earned income is generally pay you receive for personal services or work that you perform in a foreign country, such as wages, salaries, or professional fees. Now, foreign earned income does not include certain items.

⇒ It doesn’t include the value of meals and lodging that you exclude from your income because they were furnished for the convenience of your employer.

⇒ It doesn’t include pension or annuity payments you receive, including social security benefits. If you receive pay as a U.S. government employee, the pay you receive as a government employee is not eligible for the foreign earned income exclusion.

⇒ You also can’t exclude amounts you include in your income because of your employer’s contributions to a nonexempt employee trust or to a nonqualified annuity contract, or any unallowable moving expense deductions that you choose to recapture, and you cannot exclude payments you receive after the end of the tax year following the tax year in which you performed the services that earned the income.

You must also have a foreign tax home. Your tax home is the general area of your main place of business, employment, or post to duty regardless of where you maintain your family home. Your tax home is the place where you are permanently or definitely engaged to work as an employee or self-employed individual. Having a tax home in a given location does not necessarily mean that the given location is your residence or domicile for tax purposes. Now, if you don’t have a regular main place of business because of the nature of your work, your tax home may be the place where you regularly live. If you have neither a regular or main place of business, nor a place where you regularly live, you’re considered an itinerant, and your tax home is wherever you work. Now there is one condition. You are not considered to have a tax home in a foreign country for any period in which your abode is in the United States.

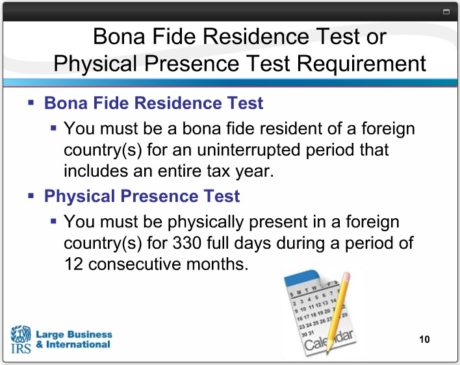

So, in addition to having foreign income and a foreign tax home, you must also meet the bona fide residence test or the physical presence test. You meet the bona fide residence test if you are a bona fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year. You do not automatically acquire bona fide residence status merely by living in a foreign country or countries for a year or more. If you go to a foreign country to work on a particular job for a specified period of time, you ordinarily will not be regarded as a bona fide resident of that country, even though you worked there for one tax year longer. The length of your stay and the nature of your job are only two of the factors to be considered in determining whether or not you meet the bona fide residence test. You meet the physical presence test if you are physically present in a foreign country or countries for 330 full days during a period of 12 consecutive months. A full day is a period of 24 consecutive hours beginning at midnight. The 330 days do not have to be consecutive.

You can count days that you spent abroad for any reason. You don’t have to be in the foreign country only for employment purposes. You can be on vacation. Unlike the tax home test, this test does not depend on the kind of residence you establish, your intentions about returning to the U.S., or the nature and purpose of your stay abroad.

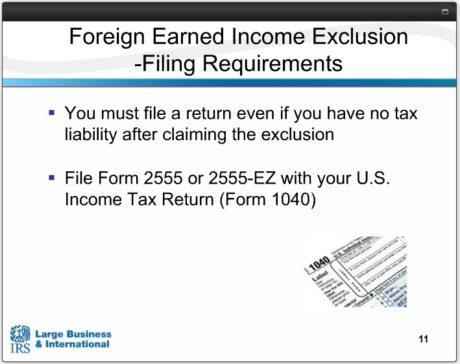

If you meet the qualifications for the foreign earned income exclusion, you must file U.S. income tax returns, even if you have no tax liability after claiming the exclusion. You must attach either Form 2555 or 2555-EZ to your U.S. income tax return to claim the foreign earned income exclusion.

If you are claiming either the foreign housing exclusion or the foreign housing deduction, you cannot file the Form 2555-EZ. You have to file the Form 2555. Form 2555 shows you how you qualify for the bone fide residence test or physical presence test, how much of your earned income is excluded, and how to figure the amount of your allowable housing exclusion or deduction. Form 2555-EZ is a simpler version of the form that has fewer lines. You can use this form if all seven of the following requirements are met:

⇒ First, you have to be a U.S. citizen or resident alien.

⇒ Next, your total foreign earned income for the year is not more than the maximum foreign earned income exclusion for the corresponding tax year.

⇒ You must have earned wages or salaries in a foreign country.

⇒ You must be filing a calendar year return that covers a full 12-month period. You cannot have any self-employment income for the year.

⇒ You cannot claim any business or moving expenses for the year, and you’re not going to be claiming the foreign housing exclusion or deduction.

So if you meet those, you can file the 2555-EZ, otherwise you need to file the Form 2555.

The maximum foreign earned income exclusion is adjusted annually for inflation. For 2016, the maximum exclusion amount has increased to “$101,300.” You cannot exclude more than the smaller of “$101,300” or your foreign earned income for the tax year minus your foreign housing exclusion amount. If both you and your spouse work abroad and both of you individually meet the requirements for claiming the foreign earned income exclusion, you can each choose the foreign earned income exclusion. If this is the case, both you and your spouse must each file a separate Form 2555 or 2555-EZ. So in other words, if you’re filing a joint return and both you and your spouse qualify for the foreign earned income exclusion, you will have two Form 2555 attached and two $101,300 amounts.

In addition to the foreign earned income exclusion, you can also claim an exclusion or deduction from gross income for your housing amount if your tax home is in a foreign country and you qualify for the exclusions and deductions under either the bona fide residence test or the physical presence test. The housing exclusion applies only to amounts considered paid for with employer-provided funds, which includes any amount paid to you or paid or incurred on your behalf by your employer that are taxable foreign earned income to you for that year without regard to the foreign earned income exclusion. The housing deduction applies only to amounts paid for with self-employment earnings. So if you’re not self-employed you can’t take the foreign housing deduction. Housing expenses include your reasonable expenses actually paid or incurred for housing in a foreign country for you, and if they lived with you, your spouse and dependents. Consider only housing expenses for the part of the year that you qualify for the foreign earned income exclusion when calculating the exclusion or deductions for foreign housing cost.

President

Thanks to FAS & CPA Consultants and Fulton Abraham Sanchez, CPA, I was able to resolve a debt of $479,677.71 that I had with the IRS.

Entrepreneur

My experience with FAS CPA & Consultants has been incredible, their professionalism is impeccable. I highly recommend them.

Manager

I highly recommend FAS CPA & Consultants, they are responsible, efficient and very dedicated.

Manager

How to Get a U.S. Banking License

How To Get A U.S. Banking License Email Us Today Support@fascpaconsultants.com and Get An Offshore Strategy Review I Want...

Fulton is a wonderful CPA who fully understands tax law and provides honest advice for his clients.